Insurance Coverage for Diabetes Supplies Explained

A practical breakdown of insurance coverage for diabetes supplies across Medicare, Medicaid, and private plans, plus how to appeal denials and save money.

In this article(11)

- What Insurance Coverage Diabetes Supplies Typically Includes

- Understanding the Cost of Diabetes Management Through Insurance

- Patient Assistance When Insurance Falls Short

- Saving Money Within Your Insurance Plan

- What Does Insurance Cover for Diabetes Testing Supplies

- Navigating Coverage for Advanced Devices

You open the pharmacy bag, glance at the receipt, and feel that small drop in your stomach when the number is higher than you expected. Insurance coverage diabetes supplies decisions get made by a system that rarely explains itself at the counter, and the rules shift between plans, states, supply categories, and even the season your deductible resets. Knowing what your plan covers, and what it should cover by law, can quietly save you hundreds or even thousands of dollars across a year.

We hear the same questions over and over from the Diabic community. People are not confused because they are uninformed. They are confused because the rules are genuinely tangled, and pharmacy counter staff often do not have time to walk through them. This guide is the conversation we wish someone had with us the first time we tried to fill a script for test strips on a new plan.

We will break down what most plans cover, how Medicare and Medicaid differ from private insurance, where the hidden costs live, and what to do when a coverage denial lands in your inbox. None of this replaces a call to your plan, but it should help you make that call a much shorter one.

From my experience: When I switched plans in 2022, my Dexcom G6 sensors that had been pharmacy-benefit copays suddenly bounced to durable medical equipment with a separate deductible. I did not catch it until the first shipment invoice arrived, and I had to spend an afternoon on the phone reverse-engineering the routing. The lesson I keep relearning: any time anything changes (plan, employer, even calendar year), call member services before the refill, not after.

What Insurance Coverage Diabetes Supplies Typically Includes

Most health plans in the United States cover the basics that anyone with diabetes uses day to day. That usually means a blood glucose meter, test strips, lancets, lancing devices, and control solution. The American Diabetes Association maintains plan-specific resources that confirm test strips and meters fall under preventive or durable medical equipment categories on most commercial plans.

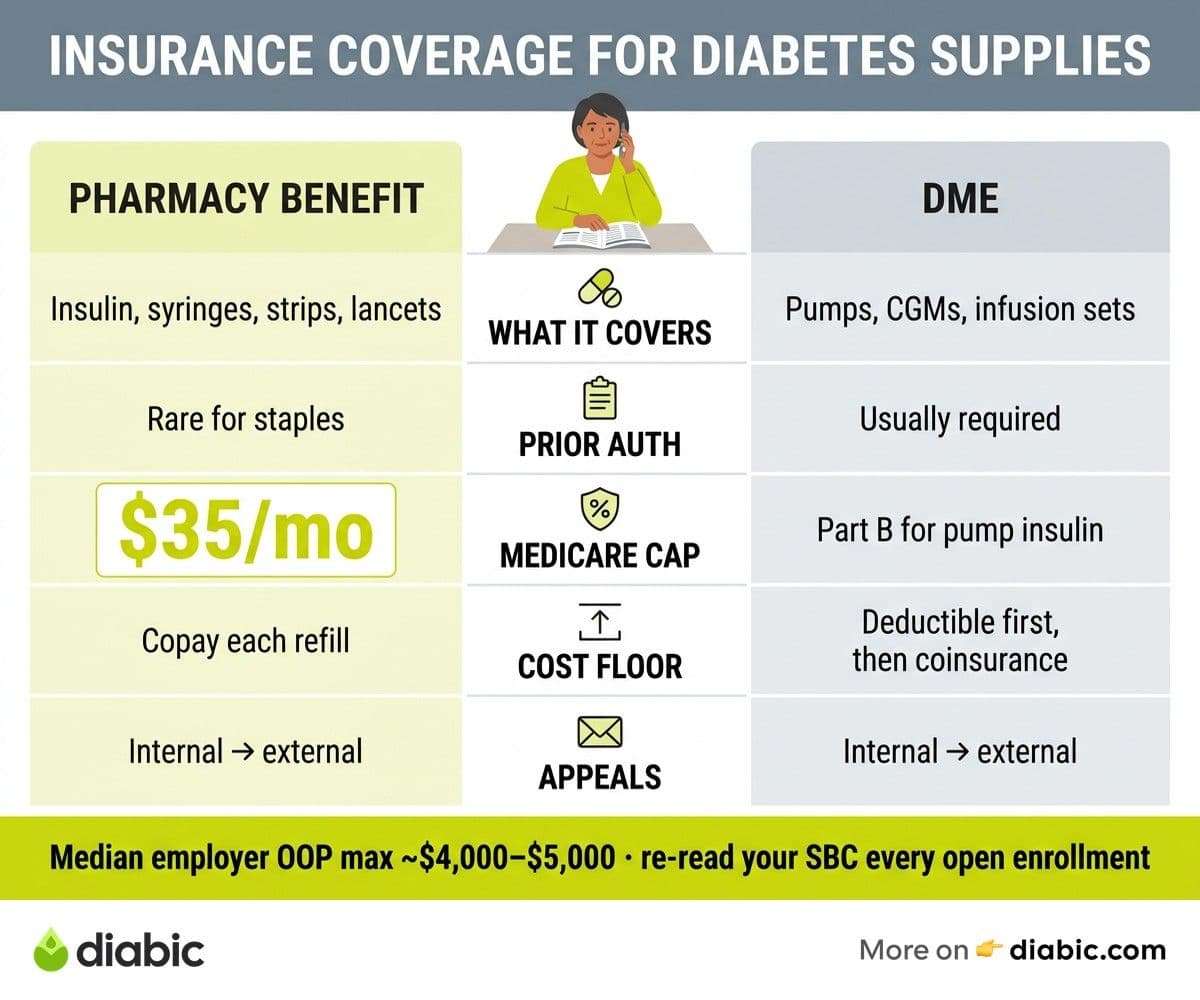

Insulin and the tools to deliver it sit in a separate bucket. Vials, pens, syringes, and pen needles are usually filled through your pharmacy benefit, while pumps and continuous glucose monitors often run through your durable medical equipment benefit. The split matters because the cost-sharing rules can be very different. A pen prescription might cost a flat copay, but a pump might apply against your deductible at full sticker price until you hit it.

Insulin pumps and CGMs tend to be covered when your provider documents medical necessity. For Type 1 diabetes, that documentation is fairly standard, and many plans now cover CGMs for Type 2 diabetes when insulin is part of the regimen. We have written more about the real cost of diabetes management and how device coverage shapes the total picture, because the headline price of a CGM rarely matches what you actually pay.

Diabetes self-management education and medical nutrition therapy are often the most overlooked benefits on a plan. Under the Affordable Care Act preventive services rules, many plans cover diabetes screening and counseling at no cost share, and Medicare covers up to ten hours of initial diabetes self-management training. Ask your plan whether your annual visit with a certified diabetes care and education specialist is covered, because the answer is yes more often than people assume.

Understanding the Cost of Diabetes Management Through Insurance

The cost of diabetes management on insurance comes from four moving parts: your premium, deductible, copays or coinsurance, and out-of-pocket maximum. Premiums are predictable, but the other three drive the surprises. A high-deductible plan might look cheap on paper, then ask you to pay full retail for a month of pump supplies in January before any benefit kicks in.

In-network and out-of-network status changes the math at every step. Some specialty pharmacies that ship pump supplies are in network for one plan and out of network for another, even when both plans share a brand name. Before you re-order, log in to your plan portal and verify that the supplier listed on your last shipment is still preferred. Suppliers get dropped quietly, and the first sign is sometimes a denied claim.

High-deductible plans paired with a health savings account can work well if you are deliberate about it. You can pay for test strips, insulin, lancets, and pump supplies with pre-tax dollars, which effectively cuts the price by your marginal tax rate. The catch is cash flow, because you front the cost until you can reimburse yourself from the HSA. Many people set aside a sinking fund in January so a surprise pump infusion-set order does not land on a credit card.

The out-of-pocket maximum is the friend most people forget about. Once you hit it, most plans cover in-network supplies at one hundred percent for the rest of the year. If you know you will hit your max regardless, it can make sense to schedule elective items, like a backup meter or extra pump supplies, before the calendar resets. According to KFF analysis, the median out-of-pocket maximum on employer plans now sits around four to five thousand dollars, which is meaningful but reachable for many people on insulin therapy.

Patient Assistance When Insurance Falls Short

Even on a decent plan, gaps happen. A formulary changes mid-year, a prior authorization stalls, or a job change leaves you uninsured for sixty days. This is where patient assistance programs do quiet but important work. Most major insulin makers run copay cards or free-product programs with income thresholds that are more generous than people expect.

Manufacturer copay cards from Eli Lilly, Novo Nordisk, and Sanofi can bring monthly insulin costs down to thirty-five dollars or less for people with commercial insurance. These cards usually do not work with Medicare or Medicaid, which is a federal restriction rather than a manufacturer choice. Patient assistance programs from the same companies often provide free insulin to people who meet income limits, regardless of insurance status. We cover specifics in our piece on patient assistance programs for diabetes medication.

State pharmaceutical assistance programs fill another gap. About a dozen states run programs that subsidize prescription costs for low-income residents, often layered on top of Medicare or Medicaid. The National Conference of State Legislatures keeps a current list of these programs, and eligibility rules vary widely. If you live in New York, Pennsylvania, New Jersey, or several other states, the savings can be substantial.

Non-profits also step in when manufacturer programs do not match your situation. Organizations like the Lions Club, Mutual Aid Diabetes, and Beyond Type 1 connect people to short-term emergency supplies. If you are forty-eight hours away from running out of insulin, your local community health center or federally qualified health center can often provide a bridge supply. We mention this not to alarm you, but because the second-worst time to learn these resources exist is during a crisis.

Saving Money Within Your Insurance Plan

Even within a plan you cannot change, there is room to lower the price you pay. Preferred pharmacies often have negotiated rates that walk-up customers do not see. Mail-order pharmacies, when your plan offers them, frequently knock thirty to fifty percent off ninety-day fills compared to thirty-day retail pickups. The savings come from a single dispensing fee instead of three, and from supply chain economics that favor longer fills.

A few specific moves consistently lower costs for our community:

- Switch to ninety-day fills for stable medications and test strips, which most plans price at two copays instead of three for the same volume of product.

- Ask your prescriber to write for the highest-quantity unit your plan allows, especially for pen boxes, so you avoid frequent refill copays.

- Compare your insurance copay to the cash price at GoodRx or your pharmacy's discount card, because cash sometimes beats insurance on test strips and metformin.

- Use a single in-network pharmacy whenever possible, because many plans tier their preferred network with deeper discounts at one chain.

Appeals are the most underused tool in the system. When a plan denies a CGM, pump, or new insulin, the first denial is rarely the final word. Federal rules under the ACA give you the right to an internal appeal and, if that fails, an external review by an independent third party. Your prescriber's office usually has a denial letter template, and the timeline matters because most plans require appeals within sixty or one hundred eighty days of the denial. We collect more tactics in our guide to diabetes supply savings strategies.

What Does Insurance Cover for Diabetes Testing Supplies

Federal and state mandates create a coverage floor that most plans cannot drop below. The ACA classifies diabetes screening as a preventive service, which means many plans cover the screening visit and lab work with no cost share. Beyond screening, most states have additional mandates that require commercial plans to cover insulin, syringes, test strips, and meters at standard cost-sharing levels. The specifics vary, so the NCSL state legislation tracker is worth checking for your state.

Medicare Part B covers diabetes testing supplies for people who use insulin and people who do not, though the quantities differ. Through 2024 and into 2025, Medicare also caps out-of-pocket insulin costs at thirty-five dollars per month for covered insulins under both Part B and Part D, a change that came from the Inflation Reduction Act. CGMs are covered under Part B for people with Type 1 or insulin-treated Type 2 diabetes when prescribed by a Medicare-enrolled provider.

Medicaid coverage varies more than any other category because each state administers its own program. All state Medicaid programs cover insulin and basic testing supplies, but the preferred brands, quantity limits, and prior authorization requirements differ. The Centers for Medicare and Medicaid Services maintains state plan documents that show what your state covers, and your state Medicaid hotline can confirm specifics for your enrollment.

If you have employer-sponsored coverage, your summary of benefits and coverage document is the legally required short-form summary of what is covered. Plan documents are dense, but the SBC is usually four pages and includes a sample diabetes scenario. Reading yours once a year, especially during open enrollment, is the single highest-uses thing you can do for your supply costs.

Navigating Coverage for Advanced Devices

CGMs and insulin pumps live in their own coverage world, mostly because they are durable medical equipment rather than pharmacy items. Coverage criteria almost always require prior authorization, and the documentation standards are specific. For CGMs, plans typically want recent A1C values, evidence of multiple daily insulin injections or pump use, and a statement of medical necessity from your prescriber. For pumps, the bar is similar, often with additional requirements about hypoglycemia history or A1C goals.

Prior authorization is paperwork, but it is paperwork your prescriber's office handles dozens of times a week. The fastest path is to bring the requested device's manufacturer-provided letter of medical necessity template to your appointment. Dexcom, Abbott, Tandem, Insulet, and Medtronic all maintain these on their professional sites, and they often include the exact ICD-10 codes and clinical language that plans expect.

Smart insulin pens are a newer category, and coverage is uneven. Some plans treat them as durable medical equipment, others as pharmacy items, and a few do not cover them at all. If your prescriber recommends a smart pen, ask them to write the script and submit it through both the pharmacy and DME channels, because the first denial is sometimes just routing confusion. The FDA device database lists current cleared devices if you want to verify regulatory status before requesting coverage.

When you build a case for coverage, the strongest documentation pairs your numbers with a clinical narrative. A note that says "patient has experienced three documented episodes of severe hypoglycemia in the past six months and would benefit from continuous glucose monitoring to reduce risk" carries more weight than a generic letter. Your provider has seen this play before, but you can speed things up by sharing your CGM data, finger-stick logs, or pump-readiness checklist when you ask.

FAQ

Does insurance cover diabetes testing supplies?

Most health insurance plans are required to cover basic diabetes testing supplies, including blood glucose meters, test strips, and lancets, under federal preventive services rules and a layer of state mandates. The amount of coverage, preferred brands, quantity limits, and your share of the cost vary between plans, so checking your summary of benefits and your plan formulary is the fastest way to know what applies to you.

What diabetes supplies are covered by insurance?

Typically covered supplies include glucose meters, test strips, lancets, insulin, syringes, pen needles, and ketone strips for people on insulin. Many plans also cover insulin pumps and CGMs with prior authorization, and most cover diabetes self-management education and medical nutrition therapy. Smart pens and newer accessories vary by plan, so a quick call to member services with the exact product name and HCPCS code is worth the time.

How do I appeal a coverage denial for diabetes supplies?

Start with the denial letter, which must include the reason for denial and the appeal deadline by federal law. File an internal appeal first, with a letter of medical necessity from your prescriber and any supporting clinical records. If that fails, request an external review by an independent reviewer, which is your right under the ACA for most denials. Most appeals are resolved within thirty to sixty days, and many succeed on the first internal round when documentation is complete.

Does Medicare cover insulin and CGMs?

Yes. Medicare Part D covers most insulins with a thirty-five-dollar monthly cap on covered products, and Part B covers insulin used through a pump along with pump supplies. CGMs are covered under Part B for beneficiaries who meet clinical criteria, including people on multiple daily insulin injections or pump therapy.

The honest summary is that insurance coverage diabetes supplies rules reward the people who keep their plan documents nearby and ask one extra question at the pharmacy. A five-minute call to member services before a refill, a quick check of your formulary at open enrollment, and a willingness to appeal a denial are usually what separates a year of surprise bills from a year of predictable costs. Bring your prescriber and pharmacist into the loop early, because they see these patterns weekly and can flag a switch before it shows up on your card. None of this should be your full-time job, but a little upfront attention to insurance coverage diabetes supplies decisions tends to pay back many times over.

Shahriar P. Shuvo is the founder of Diabic. He has lived with diabetes for over 14 years, and built Diabic to deliver the practical, evidence-based self-management tools he wished existed when he was first diagnosed. By trade, Shahriar is a senior design and frontend engineer with 6+ years shipping products at Agora, Timescale (now Tiger Data), and ShareTrip. He writes from the intersection of lived diabetes experience and product craft, focused on what works in daily management rather than what sounds good in a textbook.

Medically reviewed by

Dr. Shanto Arian is an internal medicine physician now specializing in clinical and aesthetic dermatology, with a parallel academic focus on epidemiology and public health. He holds an MBBS, MPH, MSc (UK), MRCP (UK), MRCPI (Ireland), Diploma in Dermatology (UK), and Diploma in Aesthetic Medicine (USA). Dr. Arian trained in internal medicine, including hospital work on hematology cases such as graft-versus-host disease, before moving toward dermatology. Skin is one of the earliest places diabetes shows itself, from acanthosis nigricans and diabetic dermopathy to slow foot wound healing, and that intersection is where his clinical and Diabic-review work meet. On Diabic, Dr. Arian medically reviews content on diabetes diagnosis, complications, dermatologic manifestations, and pharmacotherapy, ensuring every claim aligns with current ADA, NICE, and peer-reviewed literature.

More from Living with Diabetes

View all

Generic vs Brand Insulin: Is There a Difference?

Generic vs brand insulin compared: how biosimilars are approved, what you save with Semglee or ReliOn, and how to talk to your doctor about switching.

Patient Assistance Programs for Diabetes Medication

Patient assistance programs diabetes patients qualify for can cut prescription costs to little or nothing. Here is how to find and apply for them.

Diabetes Supply Savings Tips That Actually Work in Real Life

Practical diabetes supply savings tips for cutting costs on test strips, CGMs, insulin, and pump supplies without compromising your care.

Clinician-reviewed habits, plain-language guides, and honest answers - the small shifts that make living with diabetes feel lighter, every day.