The Real Cost of Diabetes Management

The real cost of diabetes management goes far beyond insulin and test strips. Here is the full picture and practical ways to lower the total.

In this article(11)

The cost of diabetes management is one of the least discussed parts of living with this condition, partly because the full number is genuinely uncomfortable to look at. When most people think about the price of diabetes, they think about insulin, maybe test strips, maybe a doctor visit or two. The real picture includes specialist appointments, dental cleanings, eye exams, foot care, dietary upgrades, mental health support, and the income lost to sick days, and it adds up fast.

We want to be honest with you about what this actually costs, because pretending otherwise does not help anyone manage their finances or their health. Diabetes is expensive, and the expense is not your fault. What we can do is map out where the money goes, where the system has gaps, and where you have uses to bring the total down. This is the conversation we wish someone had with us early on, and we hope it is useful to you now.

From my experience: When I switched to a Dexcom G6 around 2019, the monthly sensor cost felt manageable until my plan reset in January and I hit the deductible cliff. I remember staring at a $400 pharmacy receipt for three sensors and a vial of Humalog, doing the math in my head, and realizing I had budgeted for the wrong month. Now I treat January and February as a separate line item every year.

Breaking Down the Cost of Diabetes Management

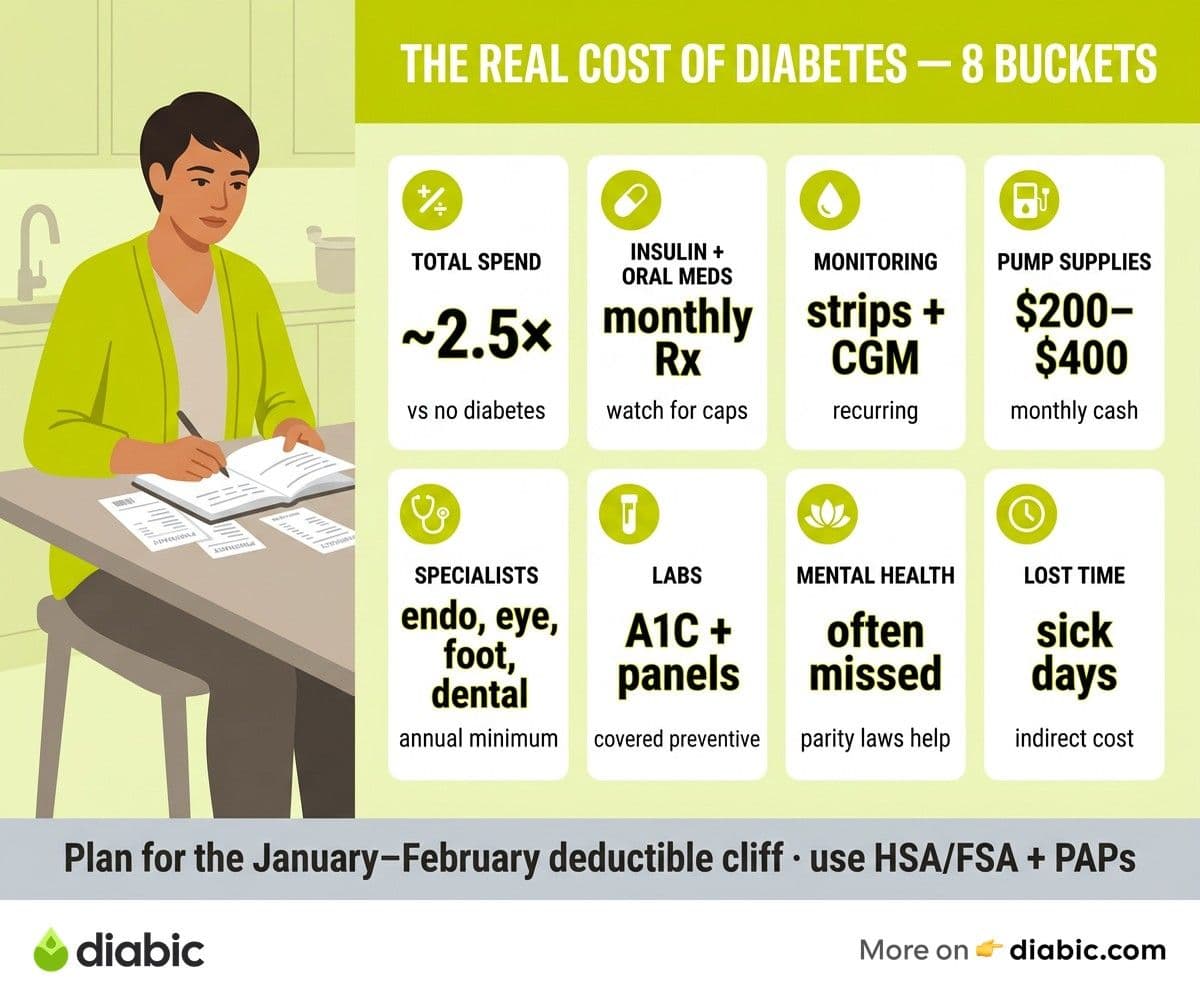

According to the American Diabetes Association's Economic Costs of Diabetes report, the average person diagnosed with diabetes spends roughly two and a half times more on medical care each year than someone without diabetes. The total annual economic cost of diabetes in the United States runs into the hundreds of billions of dollars, with the majority falling on the people who live with the condition and their families. These figures are sobering, but they help put your own bills in context.

Direct medical costs are the ones most people picture first, and they include medications, blood glucose supplies, doctor visits, lab work, and the occasional emergency room trip. For a person with type 2 diabetes managed with oral medications, these costs run lower than for someone with type 1 diabetes who uses insulin, a continuous glucose monitor, and an insulin pump. Both can still consume a significant share of annual income, especially when high deductibles or limited formularies push more spending into your out-of-pocket column.

Indirect costs are the ones that quietly inflate the total without showing up on a single bill. Missed work for medical appointments, reduced productivity during high or low blood sugar episodes, time spent on hold with insurance companies, and the mental load of constant decision-making all carry an economic price even when no money changes hands. Researchers tracking these effects through the Centers for Disease Control and Prevention have found that lost productivity contributes substantially to the overall societal burden of diabetes, and individuals feel it personally in smaller paychecks and burned-out evenings.

Type 1 and type 2 diabetes carry different cost profiles, and that matters when you are budgeting. Type 1 management almost always involves insulin and is more equipment-heavy, with pumps, CGMs, and pump supplies forming the backbone of daily care. Type 2 costs vary much more widely depending on whether the person is using insulin, GLP-1 medications, or older oral drugs like metformin. Both populations face similar long-term complications and screening costs, which we will get to shortly.

Diabetes Supply Costs: Where the Money Goes

Test strips have a quiet way of draining a budget, and they often cost more in cash terms than people expect. Even with insurance, the copay on a month's supply can run into the dozens of dollars, and uninsured cash prices climb higher. Lancets and alcohol swabs add a smaller but persistent line item to the monthly total. Our guide to practical supply savings tips digs into specific tactics for keeping these recurring costs in check.

Continuous glucose monitors and insulin pumps are where supply costs really compound. A CGM sensor typically lasts ten to fourteen days and is replaced on a regular cycle, while pump infusion sets and reservoirs need swapping every few days. With insurance, durable medical equipment coverage can offset much of this, but coinsurance percentages and deductibles often leave a meaningful balance. Without insurance, these technologies can be effectively out of reach unless you tap into manufacturer financial assistance or used-equipment communities.

The smaller items deserve attention too, because they are easy to underestimate. Ketone strips, glucose tablets for treating lows, sharps containers, batteries for older meters, and over-the-counter aids like alcohol prep pads each cost only a little, but they recur every month for the rest of your life. When we add up annual supply costs for typical management profiles, we routinely see four-figure totals for type 2 diabetes managed with finger sticks alone, and substantially higher numbers for anyone using a CGM and insulin pump. Insurance generally covers a meaningful share, but the gap between covered and out-of-pocket is rarely zero.

Insurance and What It Actually Covers

Insurance is supposed to take the edge off these costs, and to a real extent it does, but the gap between what your plan covers and what you actually pay is wider than most people expect. High-deductible health plans have become increasingly common, and they can leave you paying full price for medications and supplies until you hit a deductible that often exceeds a few thousand dollars. For someone with diabetes, that deductible typically gets met early in the year, but the first quarter's bills can be brutal.

Specialty tier formularies are another quiet trap. Newer diabetes medications, including many GLP-1 receptor agonists and some long-acting insulins, are placed on tiers with high coinsurance percentages rather than fixed copays. A medication with a forty percent coinsurance can cost hundreds of dollars per fill even with insurance, and these costs often surprise people at the pharmacy counter. The Kaiser Family Foundation tracks these trends in detail and has documented how out-of-pocket spending for chronic conditions has shifted onto patients over the past decade.

Out-of-network surprises hit particularly hard around diabetes care because management often involves multiple specialists. Endocrinologists, ophthalmologists, podiatrists, dietitians, and certified diabetes care and education specialists may not all be in the same network, and a single visit to the wrong provider can add hundreds of unreimbursed dollars to your bill. Calling ahead to confirm network status, even when your primary doctor referred you, has saved us and many readers from bills we were not expecting. For a more thorough breakdown of where coverage tends to fall short, see our piece on insurance coverage for diabetes supplies.

Marketplace plans purchased through Healthcare.gov vary significantly in how they cover diabetes care, and choosing the right metal tier can make a meaningful difference in your annual spend. A plan with a higher monthly premium but lower deductibles and copays often pencils out better for someone with diabetes than a cheaper plan with a high deductible, even though the cheaper plan looks more attractive at first glance. Running the math with your actual prescription list before enrollment is one of the highest-uses financial moves you can make in any given year.

Affordable Insulin and Medication Costs

Insulin pricing in the United States has been the subject of intense scrutiny over the past decade, and recent legislative changes have created caps for some patients while leaving others paying historical prices. Medicare beneficiaries now have monthly insulin cost caps under federal law, and several states have passed their own caps for state-regulated commercial plans. Despite these reforms, uninsured patients and those on plans not covered by the caps can still face full retail prices, which is why manufacturer assistance remains so important.

Brand-name versus generic comparisons get complicated quickly with diabetes medications. Metformin is widely available as a low-cost generic, and many older sulfonylureas are similarly affordable. Newer classes including GLP-1 receptor agonists, SGLT2 inhibitors, and DPP-4 inhibitors are still primarily branded, with cash prices that can exceed several hundred dollars per month. Authorized generics and biosimilar insulins have started to appear and have lowered some prices, though access varies by pharmacy and insurer.

Combination therapies multiply costs, since many people with diabetes take three, four, or more medications when you include drugs for blood pressure, cholesterol, and other related conditions. Each prescription carries its own copay or cash price, and the cumulative monthly total is what most patients feel rather than any single line item. Looking at affordable insulin options and exploring whether you qualify for manufacturer programs can take a meaningful chunk out of this number, often cutting one of the largest individual costs to a fraction of what you currently pay.

Hidden Costs Most People Miss

Dental care is often overlooked in diabetes budgeting, but people with diabetes face higher rates of gum disease and tooth loss documented by NIDDK, and dental insurance is famously thin in what it covers. Annual cleanings are non-negotiable for oral health, and treatment for periodontitis or extractions can cost thousands of dollars per episode. Many endocrinologists now ask about dental visits at every appointment for exactly this reason, and we encourage you to budget for it as part of your diabetes care, not as a separate expense.

Eye exams are similarly essential and often surprisingly expensive. Annual dilated eye exams with retinopathy screening are recommended for everyone with diabetes, and depending on your vision plan, the screening portion may be covered while the regular exam comes out of pocket, or vice versa. Treatment for diabetic retinopathy, when needed, can involve injections or laser procedures that run into thousands of dollars per session, even with strong coverage.

Foot care, including podiatry visits and properly fitted footwear, deserves a place in your annual budget. Medicare and many private plans cover therapeutic shoes and inserts for people with diabetes who meet specific criteria, but the application process requires documentation from your provider. Routine podiatry visits for nail care and skin checks are often covered for people with diabetic neuropathy, and we strongly encourage using these benefits when you have them. Catching problems early prevents the much larger costs of foot ulcers and infections.

Mental health support is another frequently missed expense. Diabetes distress and depression are common in people managing this condition, and therapy or psychiatric care can be expensive when not well covered. Many insurance plans have improved mental health coverage following parity laws, but copays and limited in-network options still create barriers. Sliding-scale clinics, employee assistance programs, and online therapy platforms can fill some of the gap.

Dietary changes also carry a real cost. Buying more whole foods, fresh produce, lean proteins, and lower-glycemic ingredients often costs more per meal than relying on processed alternatives, even though the long-term health math favors the better diet. Budgeting for this and using strategies like seasonal produce, frozen vegetables, and bulk staples helps keep the grocery line item from ballooning.

Strategies to Reduce the Financial Burden

The single highest-uses move for most people is exploring patient assistance programs, especially for insulin and newer medications. Manufacturer programs from Lilly, Novo Nordisk, and Sanofi can reduce or eliminate insulin costs for people who qualify, and similar programs exist for many oral and injectable diabetes medications. Our deep dive into patient assistance programs walks through eligibility, application steps, and emergency provisions in detail.

Tax-advantaged health accounts offer real savings if you have access to them. Health Savings Accounts, available with high-deductible plans, let you set aside pre-tax dollars for medical expenses and roll the balance forward indefinitely. Flexible Spending Accounts work similarly but typically use a use-it-or-lose-it model. Both can cover most diabetes-related expenses, including supplies, copays, and even some over-the-counter items. Medical expense tax deductions are also available for people whose total qualifying medical costs exceed a percentage of their adjusted gross income, with details outlined in IRS guidance.

Comparing pharmacy prices is worth more than most people realize. Cash prices for the same medication can vary substantially between chain pharmacies, independent pharmacies, and mail-order options, and discount card programs sometimes beat insurance pricing for specific drugs. Asking your pharmacist directly whether the cash price is lower than your copay is a normal question, and the answer is sometimes yes. For another angle on bringing down recurring costs, our guide on affordable insulin options maps out specific paths.

Negotiating with providers and pharmacies is a less-explored option that occasionally works. Hospital billing departments often have financial assistance policies that can reduce or eliminate balances for patients who apply, and pharmacy chains sometimes offer in-house discount programs that staff will mention only if asked. Community resources, including diabetes nonprofits, religious organizations, and local health departments, can fill gaps for specific situations like emergency supplies or one-time copay assistance.

FAQ

How much does diabetes management cost per year?

According to the American Diabetes Association, average annual direct medical costs for a person with diabetes run roughly two to three times higher than for someone without the condition. Out-of-pocket costs vary widely based on insurance coverage, medication needs, and supply use. Type 1 diabetes generally costs more annually due to insulin, CGM, and pump expenses, while type 2 costs depend heavily on whether insulin or branded medications are part of the regimen.

How can you reduce the cost of managing diabetes effectively?

Use patient assistance programs for medications, switch to generic versions where clinically appropriate, compare cash prices across pharmacies, take advantage of Health Savings Accounts or Flexible Spending Accounts, and ask your healthcare team about cost-effective alternatives for both medications and supplies. Tax deductions for medical expenses can also help if your annual costs cross the qualifying threshold. Layering several small savings strategies often produces a larger reduction than any single move.

What hidden costs of diabetes do most people miss?

Dental care, eye exams, podiatry visits, mental health support, and the higher grocery cost of a whole-food diet are the most commonly missed expenses. Indirect costs like missed work and reduced productivity also add up but rarely show on a single bill. Building these into your annual budget gives you a more accurate picture of what diabetes actually costs and helps you plan rather than react.

Does insurance cover everything related to diabetes care?

No. Even strong insurance leaves gaps in areas like specialty tier medications, out-of-network specialists, dental care, and certain supplies. High-deductible plans can mean paying full price for the first several thousand dollars of care each year. Reviewing your plan's formulary and network before each enrollment period and matching it against your actual needs is one of the most valuable hours you can spend on your finances.

The cost of diabetes management is real, and naming it out loud is the first step toward bringing it under control. Insurance, assistance programs, smart shopping, and tax-advantaged accounts each take a slice off the top, and combining several of them can meaningfully change what you spend in a year. You did not cause this expense, and you do not have to absorb it without support. Take the time to map your own numbers, look for the leverage points that apply to your situation, and use the resources built specifically for people in this position.

Shahriar P. Shuvo is the founder of Diabic. He has lived with diabetes for over 14 years, and built Diabic to deliver the practical, evidence-based self-management tools he wished existed when he was first diagnosed. By trade, Shahriar is a senior design and frontend engineer with 6+ years shipping products at Agora, Timescale (now Tiger Data), and ShareTrip. He writes from the intersection of lived diabetes experience and product craft, focused on what works in daily management rather than what sounds good in a textbook.

Medically reviewed by

Dr. Rezwana Parvin Rumpa is an obstetrics and gynaecology specialist with clinical focus on gestational diabetes, PCOS, and fertility. She holds the MRCOG (Final Part) from the Royal College of Obstetricians and Gynaecologists in London, the MRCPI (Final Part) from the Royal College of Physicians of Ireland, and an MBBS from Shaheed Monsur Ali Medical College under Dhaka University. Dr. Rumpa serves as a Senior Medical Officer in the Obs and Gynae department at BRB Hospitals Ltd, where she has spent three years managing prenatal care, emergency obstetric cases, and women's-health surgery. On Diabic, she medically reviews content for women living with diabetes, with particular attention to pregnancy, PCOS, and reproductive-health intersections.

More from Living with Diabetes

View all

Generic vs Brand Insulin: Is There a Difference?

Generic vs brand insulin compared: how biosimilars are approved, what you save with Semglee or ReliOn, and how to talk to your doctor about switching.

Patient Assistance Programs for Diabetes Medication

Patient assistance programs diabetes patients qualify for can cut prescription costs to little or nothing. Here is how to find and apply for them.

Diabetes Supply Savings Tips That Actually Work in Real Life

Practical diabetes supply savings tips for cutting costs on test strips, CGMs, insulin, and pump supplies without compromising your care.

Clinician-reviewed habits, plain-language guides, and honest answers - the small shifts that make living with diabetes feel lighter, every day.